The interest rates set by the Federal Reserve Bank have been pegged near zero for many years now, and investors are signalling that they are ready to see it go up.

During the financial crisis, interest rates were slashed down to historic low levels as the Fed did everything in its power to ease lending and help spur the economy back into recovery. Beyond cutting interest rates, the Fed embarked on other programs, such as bond-buying, to try to inject more cash into the economy. However, as markets improved, it has been trying to find a way to start backing out of its “emergency” position.

The bond-buying program of “Quantitative Easing” ended several months ago, but they still have not been able to raise interest rates back to “normal” levels. One major reason is that there has not been enough inflationary pressure to justify it, but another major concern is that the shock of raising interest rates could hurt growth as money becomes more expensive to borrow.

However, the bonds market, the leading indicator as to how the market as a whole will react to changes in interest rates, is holding steady ahead of next week’s meeting, where most analysts expect the rates to finally start to rise. Bond investors are the most sensitive to interest rate changes; as the interest rates on government bonds change, the yields bond investors rely on are impacted directly. Stable bond markets ahead of potential interest rate increases sends a strong signal that the markets are ready for what the Fed throws at them.

If you want to get exposure to bond trading on HowTheMarketWorks, you should check out some Bond ETFs! These include:

[hq]BND[/hq]: [trade]BND[/trade] and [hq]LQD[/hq]: [trade]LQD[/trade]

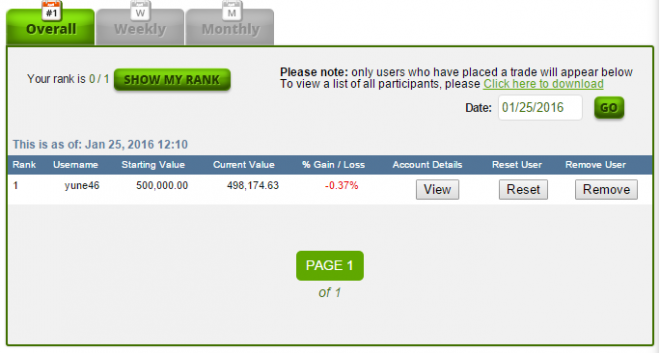

You’ve asked, and we listened! With this most recent update, teachers have more tools than ever to manage their classes on HowTheMarketWorks. You can access all these new tools from the Rankings page when you’re logged in as the contest creator.

Next to each user on the page, you have 3 new buttons: “View”, “Reset” and “Remove”. The “View” button will let you see this user’s transaction history, open positions, and an estimate of how much they made or lost on each trade. You can export all of these reports to excel too!

The “Reset” button will remove all the user’s trades and act like they have just joined for the first time. This is great if you want to give your class a “Practice Session” before starting your class contest for real.

The last button is to remove a user who joined your class by mistake. Users that have been removed cannot re-join the contest and will no longer appear in the class rankings.

We have also added a small new feature for all users – you can now quit any contest you’ve joined. The button to do so is also on the Ranking page, right next to the “Show My Rank” button.

There are many contest creators who are looking for a way to see everyone who has joined their contest, regardless of whether or not they have made a trade. We’ve added a button on the Rankings page that will download an excel spreadsheet showing all the users who have joined your contest, along with their first and last name, so it is easy to see any users who might have correctly joined your contest, but haven’t yet placed their first trade.

As always, there have been tons of small bug fixes and enhancements put on the site every week. Happy trading!

Times have been changing rather quickly for the alliance between the United States and Saudi Arabia.

The main reason is energy. US dependence on Saudi Oil has been dropping rapidly in the last decade, dropping by 50% thanks largely to increased oil production in America (if you want to try trading oil on HowTheMarketWorks, check out the [hq]OIL[/hq] ETF!). Saudi Arabia once was a major force for US policy makers to contend with; it is a leading member in OPEC, the consortium of many oil producers that coordinates production to try to ensure stable prices for its member countries, and from the mid 1970’s until very recently the United States was very depended on imported Saudi oil to keep its engines running. Many Saudi fortunes were also made when gas prices spiked in the mid-2000’s.

However, in the last few years the dynamic has been changing rapidly. The United States just has not been demanding as much oil as it used to, which is coupling with the massive drop in oil prices to have a huge impact on the Saudi budget (another popular oil ETF is [hq]USO[/hq], [trade]USO[/trade]). This comes as the United States has withdrawn troops from Iraq, and so is less reliant on Saudi military bases for supplies and logistics. There has also been tension because the Saudis would very much like the US to become more actively involved in in military campaigns in Syria, and the recent nuclear treaty with Iran, Saudi Arabia’s historical rival.

The Saudi King Salman will be in Washington today to discuss these policies and others with President Obama, but the balance of power at the table will be very different than it may have been just a few years ago.

The next 5 days will be a very important learning experience for traders trying to sift through the rubble after China’s highly-publicized currency devaluation and subsequent shockwaves through the world markets.

American markets have begun their recovery, with the S&P 500 (ETF: [hq]SPY[/hq]) and Dow-Jones (ETF: [hq]QQQ[/hq]) indecies both recovering some of the losses. However, the next few days will be critical for one big reason: the markets will not be open at the same time, so there should not be any spillover effects.

China is currently engaging in World War Two victory anniversary celebrations, closing the stock exchanges while the events take place. After that, the US markets will be closed for Labor Day, effectively segragating the actual market forces from each market to itself. This means that Chinese instability cannot cause serious intra-day trading jumps in the US, and equity flows in the US will not work for or against Chinese markets.

If you want to invest in Chinese assets on HTMW, check out the [hq]MCHI[/hq] ETF, which is heavily focused on Chinese mid-sized companies!

Stock index futures are up this morning as investors are starting to see buying opportunities after the big losses last month that stemmed from China’s stock crash and currency unrest around the world. However, investors are beginning to think that the initial sell-off was a bit of an overreaction; stock index futures are used to measure how investors feel the market will move in the near future. As investor confidence goes up, so do index futures, so when we see these kinds of increases we know the market is starting to lean towards growth.

Lots of government reports were also released today; 190,000 jobs were created in the US, although that missed the estimate of 210,000. Long-range Treasury bond yeilds moved slightly higher, but shorter-term bonds stayed the same. This usually means that the bond market thinks equities will be more attractive in the near future, but not much money has been moved from bonds into stocks just yet.

728×90 superawesome

If you want to buy into a stock index, try trading an Index ETF like SPY for the S&P 500, or QQQ for the Dow-Jones Industrial Average! Click Here for more popular Index ETFs that you can trade on HowTheMarketWorks!

Forex or (FX) is the term used for the world’s currency market. It comes from the words Foreign Exchange. Unlike stock exchanges like the New York Stock Exchange (NYSE), there is no physical location for the Forex market, instead it describes the inter-bank or Over-the-counter (OTC) market for currencies. Currencies trade 24 hours a day, five days a week (Sunday night to Friday night). Forex trading is the largest market in the world, but also has the most volatility.

Currencies are always traded in pairs; you must trade one currency vs another. For example, if we bought USD/EUR for 1.2 it would mean you need 1.2 US dollars for 1 Euro. Similarly the EUR/USD would be the inverse of that, or 1 over 1.2, meaning that to buy 1 USD you would need 0.8333 Euro.

Leverage

Forex trading is considered very risky because most Forex trading is done with 20, 50 or even 100 times margin meaning that you are exposed to a very large amount of leverage. This means that for every dollar you put down of your own money to open a position, you are borrowing another $19, $49, or $99 from your Forex brokerage.

Brokerages will loan you this money because you are trading currencies, so the value is inherent, and all of the risk is passed on to you. For example, if you have a 50 times leveraged account, if the exchange rate falls by 1%, you can lose 50% of your initial investment! You can also have the opposite case with a winning trade, but the number one priority of all investors is capital preservation; maintaining and growing the money you invest. By exposing yourself to such a high loss, you can walk away losing almost everything very quickly.

Most professional investors use an 8x or lower margin, higher amounts are usually used by beginners with very small accounts or people with many positions and want to utilize the risk of loss for the rewards.

How To Practice Trading Currencies For Free

Trading currencies takes lots of practice to get it right! There are a few ways to practice for free:

Set up a contest on HowTheMarketWorks with a different currency

Set up a trading contest on HowTheMarketWorks, but switch your currency to something else. We have over 30 to choose from, with all prices updating at the current FX rate! Once you have practiced investing in things you are familiar in using currencies you are not, you will have a better understanding of how to work with currency pairs

Use Virtual-Stock-Exchange to practice buying and selling Currency Spot Contracts

You can practice trading currencies directly, along with trading stocks and ETFs from over 30 global exchanges, by using our Global site: Virtual-Stock-Exchange. Virtual-Stock-Exchange, or VSE, works almost the exact same as HowTheMarketWorks (create your own contest, see real-time rankings, get all kinds of quote and research tools), but instead of Mutual Funds, it has Global stocks, along with currencies and some commodities (like Gold and Oil) in the form of “Spot Contracts”.

Spots are like Forex, but without the margin and leverage, so it is perfect for beginners looking to practice trading currencies.

Comparing Forex Brokers

If you want to trade forex for real, it is important not to just get practice first, but also to choose the right broker for you. There are many ways to compare forex brokers, but Australian investors have an awesome comparison tool available at https://www.compareforexbrokers.com.au.

The September Monthly Million Challenge is the first in our Monthly Million series, with over a thousand participants from all over the world! The rankings were fierce, with the HowTheMarketWorks team scattered throughout, but you’ll be surprised who won!

The Top 5 performers by portfolio value were:

AngelRivera+30.81%

Janene+23.14%

wkaraman14+18.15%

puttno2+12.63%

smithjjj5+11.19%

The HTMW Team Finishers were:

ksmith+0.12%

psimard-1.60%

Rossman-0.45%

TeamHTMW-0.64%

gbrown-24.84%

See The Trading Strategies From This Contest!

AngelRivera’s September Trading Strategy-Contest: September Monthly Million Contest Final Rank: 1 Final Portfolio Value: $1,308,146.64 (+30.8%) Trading Strategy For This Contest My strategy is finding pharmaceutical/biotech companies. I find corporations that are testing products. I look for ones who have an upcoming announcement on phase 3 testing or FDA approvals. I keep those stocks on my watchlist. Once Read More...

smithjjj5’s September Trading Strategy-Contest: Official September Contest Final Rank: 5 Final Portfolio Value: $1,119,202.95 (+11.19%) Trading Strategy For This Contest My strategy is to look for stocks to short that are moving up (30% +)on news with greater than average volume. So much of the time people get overly excited about the news and drive the price higher Read More...

wkaraman14’s September Trading Strategy-Final Rank: 3 Final Portfolio Value: $1,181,543.46 (+18.15%) Trading Strategy For This Contest I used was mainly “gap plays”; I analyze gaps in the premarket everyday, once I determine if the gap will be filled for short term investing, I will place my trade and swing looking for a 10%-20% profit. 90% of all gaps Read More...

About The Challenge

The September Monthly Million Challenge is the first in our Monthly Million series, with over a thousand participants from all over the world! The rankings were fierce, with the HowTheMarketWorks team scattered throughout, but you’ll be surprised who won!

If you missed out, you can get the details on our latest monthly challenge, where you can win cash prizes by learning about investing, on our Contests Page (Click Here)!

Prizes

Each of the top 5 portfolios won $100 Amazon gift cards!

Rules

There will be a full audit at the end of the competition on all winners to verify any corrections due to stock splits, dividends, or any other corporate action our team may have missed. Only legitimate portfolio returns will be counted in the ranking.

The usernames of the winners will be made public, but not their actual first name, last name, nor email address.

No member of the HowTheMarketWorks Team is eligable for any prizes

See The Details Of Other Contests!

Fall 2017 Challenge-Win prizes in our stock market contests! Find all of the information for any stock contests with prizes we are currently running here! You can also find information on past contests and their winners. Register Here To HTMW Fall Challenge Who can join? Anyone can join! Joining our stock market contests is completely free, so Sign Up Read More...

Back To School Challenge-Our Back To School Challenge is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! Stock Trading Contest Result Fractals7 Namburiv Catspaws Igorski123 Read More...

April Trading Contest-Our April Trading Contest is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! Stock Trading Contest Result TJack43 EddieB18 Housemanager brucehaan wolforda17 About Read More...

March Trading Contest-Our March Trading Contest is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! Stock Trading Contest Results MichaelGebhart +53.77% wpeldiak +50.55% Janene +31.00% Read More...

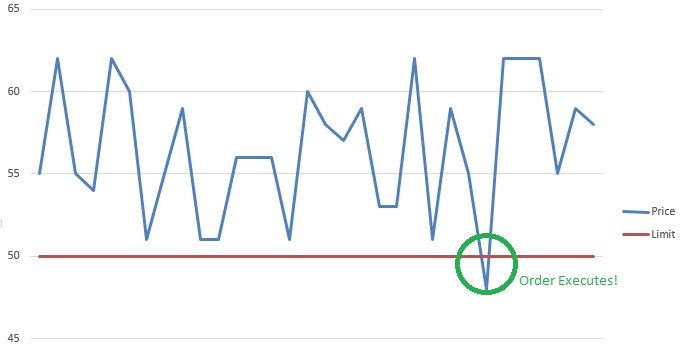

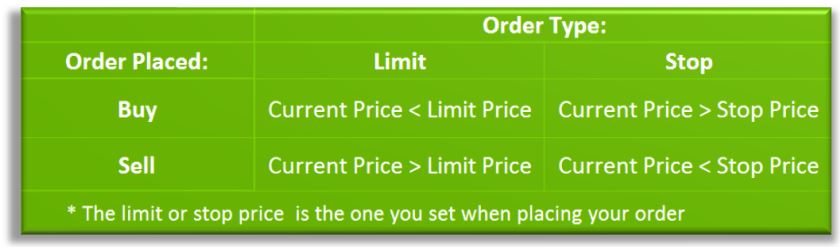

A Stop (or stop loss) order and limit order are orders that try to execute (meaning become a market order) when a certain price threshold is reached. Limit and stop orders are mirrors of each other; they have the same mechanics, but have opposite triggers.

When creating a limit or stop order, you will select a ticker symbol and quantity, just like a market order, but you will also select your target price as well. The target price is the price that triggers the limit or stop. Setting a target price does not guarantee you will get that price, it just means a market order will be created at that time. If there is not enough volume in the market to fill your order, it still may not execute.

Limit

A limit order will set the maximum price I am willing to buy (cover) at or the minimum price I am wiling to sell (short) at.

Example

Let’s say Verizon (VZ) is at $50, but you think it is overpriced and want to buy it once it falls. By setting a limit order at a target price of $45 we can wait until the price reaches that without having to sit in front of a screen. As long as the price is greater than $45 it will not execute. As soon as the price drops to $44, your stop order becomess a market order, filling at $44.

Here is a chart showing how a limit buy order works, showing a sample stock’s price over the course of a day:

A stop order will set the minimum price I am willing to sell, or short a stock. It can also mean the maximum price at which I am willing to buy, or cover.

Example

Let’s say you own PayPal stock (PYPL) that you bought at $25. If the current price is $31, you want to keep holding the stock in case the value continues to rise, but you do want to protect the gains you made.

You can put a Stop Sell order with a target price of $30, so if the price of the stock falls to $30, you will be protected from any more losses. If the value continues to rise, you will continue to hold the stock.

The table below can be an easy reminder of when a stop or limit order will execute.

Uses

Stop and limit orders will help you protect you from loss, or help you take advantage of a gain, as well as give you access to more advanced trading strategies.

One of the greatest advantages of stop and limit orders is that they can be set and left with Good Til Cancel (GTC) order expiration, and thus you don’t have to watch the stock price constantly to get well-timed trades. If prices change past your limits, the orders will execute automatically, giving you less to worry about.

This also means that you can build a much wider portfolio. If you do not need to constantly watch the price of every single one of your holdings and watchlist items because you have already set up limit and stop orders based on your preferences, you can have a much larger range of symbols on your radar.

Another important use is that you can take some of the emotion out of your trading. By setting limits and stop orders beforehand, you don’t have to panic sell or panic buy to take advantage of price swings; you already will have standing orders ready to spring into action when your pre-determined criteria are reached.

In a move that suprised almost no-one, OPEC announced that cuts in production to help prop up oil prices may soon be on the horizon.

What was surprising was that US oil producers, who are not affiliated with the group, concurrently cut back production estimates. The change in US estimates is mostly technical; instead of relying on state research and computer models, the new accounting estimates based on what actual drillers in a few key states are predicting based on the conditions on the ground.

Both cuts come at a time when oil is near its 6-year low point, oil producing countries around the world have been feeling the bite with constantly-low prices. Many oil producing countries in the Middle East are members of OPEC, an organization that works to maintain stable prices for producers. In North America, Canada and the United States are both major oil producers, with the Canadian economy being especially hard-hit by low prices and the global supply glut. In Europe, Norway is one of the biggest producers, with government officials calling the recent price crash “worse than the financial crisis” for the Norwegian economy.

Russia is the world’s leading energy exporter, and the collapse in prices has been devistating to their economy, just as sanctions from Europe over Crimea and Ukraine began over a year ago.

Alibaba (BABA) has had a wild ride since its IPO last year. Today, shares are up about 3% from the first day of trading, although that pales in comparison to the heights in November, where they hit about 75% higher than today.

Since November, prices have crashed down; their growth is still strong, but investment firms and hedge funds are having a hard time valuing the Chinese e-commerce giant. One of the major issues is how to value potential revenue growth; one of the most appealing parts to buying into fast-growing companies is also what makes them the most risky. Most of the value of the stock is rooted in how much investors expect the company to grow in subsequent years, which places a lot of value in speculation on what their market will be like 1, 3, or 5 years down the road.

Alibaba is feeling this cut now. Some of its biggest investors, large American hedge funds, are starting to dump their shares and look elsewhere, namely JD.com (ADR), which has the same market niche as Alibaba, but a very different business model, and much faster growth in the last year.

So what gives? Investors are looking for the highest return, and Alibaba is feeling the cut of changing market sentiment. JD is “Hot”, a small upstart that is gaining market share and attention quickly, while Alibaba, the darling of investors all over the world last year, is suddenly “Old News”, and needs to re-prove its worth to keep investment dollars coming in.

Yesterday index futures around the world started pushing up after China announced a cut to interest rates and banking reserve requirements. That trend continues today, with stock prices in Europe and North America pushing ahead and erasing losses from the past week. China, however, is looking at a different story.

The Shanghai Composite Index fell a further 1.3% as of Wednesday morning, with almost 5 trillion in equity erased in the last week of trading. Since June, about half the value of all Chinese stocks has disappeared. Most investors agreed that the Chinese markets, both stocks and property, have been caught in an increasingly-unstable bubble, and the massive loss in equity is a reflection of that bubble bursting. This has been made worse by bad economic news; China is looking at the lowest growth rates in decades, leading investors to further question why equity prices were rising so high in the first place.

In the near term, stocks around the world are beginning to recover, but the bad news is yet from over for China.

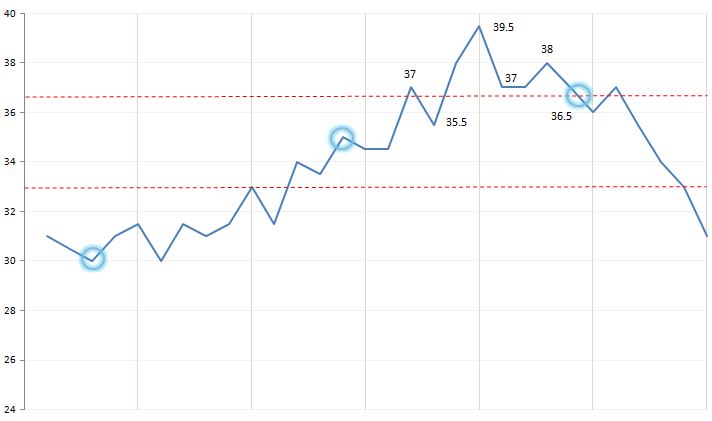

An order type that allows to set a moving stop or limit target price. The target price moves based on the daily high. Trailing stops can be set either in percentage or in dollars and cents terms. When in dollar terms it will activate when the price has moved by the target you have set relative to the day’s high.

Example

Let’s say we bought a stock for 30$. The stock then climbs to 35$. We don’t think it will go much higher but we do not want to lose our profit either. We could then set a trailing stop order for 3$. This will act just like a normal stop order. Selling at your target price. Here, however, your target (moving) price is 3$ and when the price is 35$ it will trigger at just below 32$. As we will see though, it changes based on the high:

We’ve set our trailing stop at the second bubble. Currently our selling point is 32$. The price then goes up to 37$. The new stop order will occur at 34$ (shown by the lower red dotted line). However, the price continues to go up to 39.50$ making our stop target price 36.50$ The price moves down and then back up to 38$ but this will not affect your trailing stop since it is not higher than the previous high. Thus our stop target is still 36.50$ which will be activated at which point we fall just below it.

Similarly, we could have use a percentage trailing stop. This will act just as it did previously but the target will change based on the high price. Hence if we used a 10% trailing stop in the example above. Our exit would have been at 39.50 – 10% * 39.50 = 35.55$. Percentage trailing stops can be very useful to help protect you if your price has increased considerably. For example, a 1$ trailing stop might be fine at 10$ but wouldn’t be if your stock had increased to 100$. You would be sold out of your position far too early.

Note: There are many variations that can be made with trailing stops with advanced trading software. You can change the high’s and the duration by tick size or have different ways of calculating the target price. This is far more complex however and requires a very experienced trader.

Stocks around the world this morning after the Chinese central bank announced interest rate cuts, along with lowered reserve requirements for banks to encourage banks to start lending and put a stop to the global equity selling spree.

This comes a week after the same bank drastically de-valued the Yuan, sending stocks, currencies, and futures around the world spiraling downwards. Yesterday the Dow had the biggest single-day drop in history, although it had somewhat recovered by the time trading halted.

So why cut interest rates? Central banks use interest rates and reserve requirements in their quest to constantly balance economic growth with inflation; having low interest rates makes it very cheap for people and businesses to take out loans, which can become the engine for economic growth.

Reserve requirements are what banks are required to keep in their valults and not lend out; when reserve requirements are lowered, more cash is available for banks to lend, which again can help drive growth.

However, this can come at a cost; if too many loans are taken out at the same time, it injects a lot of cash into the economy all at once, which raises prices and causes inflation. Too much inflation means that all that economic growth is lost to higher prices; instead of more economic activity, it is the same work done with bigger numbers.

These two counter-acting results mean that when the economy is strong, central banks try to raise interest rates as high as possible without hurting growth to prevent too much inflation. When the economy is weak, they lower interest rates as much as possible without causing too much inflation.

The higher the interest can get during the periods of strong growth, the more “room” the central banks have to help drive growth when the economy is weak by lowering the rates. If the interest rates are already near 0 when the economy starts to get weak, there are far fewer tools central bankers have to help get things running again.

Stocks around the world continued to lose value, over $5 trillion in value has been lost in the last 2 weeks, as investors continue to flee riskier assets after China’s currency devaluation.

The move, which many have claimed was a move designed to boost exports, has caused waves all around the world. Investment to developing countries has been especially hard hit, with Kasakhstan the first country to experience rapid inflation in its wake.

So what happened?

China devalued its currency; meaning it lowered its exchange rate compared to other countries, by over 6% in a span of a few days. From an import-export perspective, 1 US dollar now buys 6% more Chinese goods as previously, while US goods are now 6% more expensive to import to China. At this level, it works to boost Chinese exports and deter imports from other countries.

From an investor’s perspective, things look a bit different. Investors all over the world buy stocks, invest in companies, and do business in China, usually with their investments denominated in the Chinese Yuan. This means an investor from London converted his British Pounds to Yuan, and used that to buy stocks on the Shanghai Stock Exchange. From this investor’s perspective, when he eventually sells his shares, he will convert it back into Pounds.

When the exchange rate suddenly drops, it means that his investment is now worth less by exactly that amount; all of his investments in China would have just lost 6% of their value overnight. For the trillions of Dollars, Pounds, Euros, Yen, and Yuan invested from all over the world, this is a substancial loss.

This means that investors who lost value with the currency devaluation now are acting a lot more conservatively, pulling their money out of “risky” investments, and countries with less stable currencies, to try to find something more stable, like bonds. Currency traders are doing the same; trying to move all their assets out of riskier currencies. This is causing a domino effect; countries that were previously not involved, but which may have strong trading ties with China and so depend on exports to China (like Kazakhstan, which exports raw materials to China) are also getting hit both by investors pulling money out, fewer exports to China, and currency traders betting against them all at once. As more countries start to feel the sting, the panic begins to spiral outwards.

The market is still looking for a bottom, but until prices begin to stabilize, be ready for some volatility in your portfolio!

Bonds are essentially a much more formal I.O.U (I owe you) used to borrow money. You buy the bond in return to interest over a given period of time. When a corporation or government needs money they issue bonds that people buy. In turn, the issuer (the person who sells the bond) takes the money. However, no one would buy something if they didn’t get something in return, so the issuer will offer to not only pay the person back at a specified date but also provide some interest along the way.

There are two major types of bonds:

Government Bonds

These bonds are issued by governments who want to raise cash. It can be raised by any level of government; large cities often issue bonds to fund public projects, while national governments issue bonds to fund the government. When you hear about the National Debt of a country, it usually means the amount of bonds it has currently issued.

Government bonds can be traded by normal investors, but they can also be bought and sold between countries (if you hear a news pundit mention that the US government owes money to another country, like China, it is almost always because that country purchased a very large number of government bonds), or even between different parts of the government.

In the United States, the Federal Reserve buys and sells bonds from the US treasury bonds in order to influence the prevailing interest rates, for example.

Corporate Bonds

Corporations can also sell bonds, which is essentially borrowing money from a large pool of investors. Smaller companies can usually just take loans out from a bank, but if the company is very large (like Apple (AAPL), they use more cash than banks can usually give out in one single loan. Instead, they will issue bonds to investors, with a promise to pay back at a certain date with interest.

Bonds are one of two ways that companies frequently use to raise extra cash that they use for investment and expansion; the other is by issuing stocks. However, there are very important differences between the two:

If you buy a bond, you are lending money to a company and they are promising to pay you back later with interest

If you buy a stock, you are buying a part of that company and are entitled to part of its profits (in the form of dividends).

The value of the bond comes from how much you lent the company and the interest rate they will pay you back

The value of a stock comes from how much the company itself is worth (including all its assets and businesses)

Bonds expire; at the expiration date you receive back the amount you lent

Stocks do not expire

Details

Bonds can be bought and sold just like stocks, or they can be bought once and held to maturity at which point they will expire and return the face value. Essentially, when you buy a bond and hold it to maturity you will receive a certain predetermined interest rate (or coupon).

Remember that while a bond represents an amount of money that you lent to a government or company, they can still be bought or sold between investors like stocks. This means that you can buy a bond from Google (GOOG), but then later sell it to another investor who will then continue to collect the interest and receive the amount you initially lent Google when you bought the bond. Similarly, you can buy bonds from other investors rather than buying them directly from the company that issued them.

Investors typically will buy bonds when they are very risk averse, meaning they would rather have the guaranteed payment of regular interest than make riskier investments like stocks, whose value can rise and fall a lot over time.

Here a few terms that are important when looking at bonds:

Face Value

The face value, also known as par value or principal is the amount of money you will receive when the bond matures. This is almost always $1000 but there can be exceptions.

Coupon

This is the amount of interest you receive on your bond every year. It is usually stated in terms of the coupon rate (in percent). You then multiply your coupon rate by your face value, which in most cases will be $1000, to get your coupon. For example, if a bond is quoted at 4.00% you will receive $40 every year. Bonds can also be paid multiple times per year and are usually semi-annual (twice a year). In this case your coupon rate stays the same at 4.00% but you would receive two coupons of $20 instead of one coupon of $40.

Maturity

The maturity date is when the bond expires. If you are holding the bond on the maturity date then the bond Issuer will pay you the face value of the bond, which is almost always different from what you initially paid for it. In addition to the face value of the bond, if your bond had a coupon then you will also receive one final payment of whatever interest has accrued since the last payment was made. After this point the bond issuer’s debt to the bond holder is considered to be settled.

Yield

Since bonds are bought and sold between investors just like stocks, the value that they are bought and sold for on the market may not be exactly the same as the interest payments left until the bond expires and the face value. This is a very difficult concept to understand for many investors but is essentially the return you obtain when factoring the price you paid for your bond. The bond’s price is affected by the risk free rate and the bond’s own rate, as well as many other factors. The higher the Yield, the better the bond looks compared against other investments.

Accrued Interest

The interest payments on bonds are not paid daily; they are usually paid out once or twice a year (depending on the bond). However, the bond issuer owes whoever holds the bond interest for as long as they held it; if you only own a bond for a day, you are still entitled to one day of interest.

This is important for investors who buy and sell bonds a lot; if you own a bond that pays interest once per year on July 1st, but you sell it to someone else on June 15, you are entitled to most of the interest payment that they will receive from the bond issuer on July 1.

For example, lets say John bought a 5% 10 year semi-annual bond on the day it was issued and waits one year and 2 months before selling it to Kelly. This means John received two $25 coupons in the first year, and is entitled to another $8.33 from the bond issuer on top of the price he sold the bond for. This is because he held it for another two months hence 2/6 * $25 = $8.33.

Accrued Interest with Pricing

When looking at accrued interest, it has a huge impact on bond’s prices. Investors look at this in terms of a bonds dirty price and clean price. The dirty price is the price the bond trades for on the markets (if, for example, you bought a bond from another investor). This price does not subtract the accrued interest from the bond’s value. The clean price is the price with that accrued interest factored out.

Dirty Price = Clean Price + Accrued Interest

When you get a quote for a bond, you are almost always quoted the clean price, but when you buy it you will always pay the dirty price.

Rating

A rating is given to bonds to determine their level of riskiness. They are generally performed by third party auditing firms such as Standard and Poors, Moody’s or Fitch. Ratings system differ from company to company but it is important to know the difference between different bond ratings. The most common bond ratings are as follows:

AAA: Strongest Quality Rating, this has a very very low risk of default.

AA+ to AA-: Very high quality investment Grade.

A+ to BBB-: Medium quality investment grade.

BB+ to BB-: Low quality (non-investment grade) “junk bonds”, high risk of default.

CCC+ to C: Speculative bonds with very high risk of default.

D: Bonds in default for not paying principal and/or interest.

Portfolio

Nearly every balanced portfolio should have a place for bonds, if only for their strong safety while still beating inflation. Bonds can also be very risky, such as junk bonds (bonds issued by governments or companies that are very likely to not be able to pay back), that may pay high coupon rates but have a high risk of default. There are also many different types of bonds as well, such as convertible bonds that can be turned into stocks or inflation protected bonds that simply follow the rate of inflation.

Bond ETFs

You can also get exposure to bonds through bond ETF’s such as (BND) or (LQD). They have some notable differences between bonds with regards to tax considerations and returns but are much easier to trade.

Your “Risk Level” is how much risk you are willing to accept to get a certain level of reward; riskier stocks are both the ones that can lose the most or gain the most over time.

Risk

Understanding the level of risk you need and want is a very important part of selecting a good strategy. For nearly any strategy, whether it is picking stocks or doing asset allocation (picking how much of each type of investment we want) the steps in determining your level of risk are generally very similar. Determining the level of risk and reward needed is a key aspect of determining an investment strategy.

Determining your risk level

Time horizon: Your time horizon will involve when you expect to use the money you are investing.

For example, a 25 year old who is saving for retirement can go for much riskier investments since if he loses his money in a bear market, he still has a few decades to be able to make his money back. Choosing safe investments for a 25 year old would also not be a good idea since he would be losing out on the opportunity to make a lot more money. On the other hand, someone who is retiring next year will not want to risk losing his or her money if a market collapse occurs right when they retire. They would have no time to recuperate the money and could be in serious trouble, so they will want very low risk investments.

Hence, the longer your time horizon, the higher risk you can afford. The shorter the time horizon the lower risk you should choose.

liquidity: This aspect is very similar to the time horizon. Essentially someone would not choose an illiquid asset if they had needed the money for that investment in the next month. For example, real estate is considered fairly illiquid as it can take months to years to get a good price on your investment. On the other hand, popular stocks are considered very liquid as they can usually be sold anytime during market hours.

Investment knowledge: The higher your investment knowledge, the riskier the investments you can take. The reason being that you are more aware of the inherit risks and therefore more likely to make informed decisions. You would not expect someone with no investment knowledge to jump right into currency trading, they would most likely start off with mutual funds or bonds.

For example, a wall street trader will not consider futures to be as risky as someone who has never even traded a stock. The trader will know how to protect himself and have a better idea of the risks involved. It is essentially the old adage “That knowledge is Power” at work, but in this case, Knowledge is Reduced Risk.

Risk aversion: This is a measure of how comfortable you are with risk. The opposite of risk aversion is risk seeking. The level of risk aversion is usually determined by considering different scenarios and picking the one that one feels most comfortable with.

High risk aversion: You would prefer to invest in a stock that could have gains of 20% but has only lost 5% at most at a time.

Moderate risk aversion: You would prefer to invest in a stock that could have gains of 70% but also loses 20% on a regular basis.

Low risk aversion (risk seeking): You would prefer to invest in a stock that could have gains of 200% but also loses 100% on a regular basis.

Economic outlook: Unless you are following a very specific contrarian strategy, the worst the economic outlook is, the lower we would want our risk. On the other hand, a great economic outlook would allow us to increase our risk.

Savings and income: This can have a large bearing on the type of investments you will make. Someone with large amounts of savings but very little income will invest very differently from someone with a lot of income and very little savings. Again, this comes down to your individual goals. In general we would establish with our time horizon whether what our objective is. Whether we are trying to save or have income every year.

Tax Considerations: Tax considerations are a very complex matter given the large amount of differences in taxes between countries and even within. Tax breaks and savings should not be your main focus at the detriment of picking sound investments. However, it is very important to take advantage of tax breaks whenever possible when investing. Furthermore, there are usually differences between capital gains (for example a growth stock) and dividend gains (dividend stocks) which can make one or the other far more or less attractive than the other. Every location is different so it is important to educate yourself on the taxes associated with each asset.

To summarize, if investor XYZ wanted to know what his level of risk should be for his Investment strategy, he would go through each category and sum up his risk. For example, if XYZ needed his money in ten years, has moderate risk aversion, has very little investment knowledge and there is poor economic outlook. We could say his risk should be somewhere in between low and moderate.

The risk pyramid

Now that you’ve got a better idea of your risk level we can look at the types of investments that are right for that level of risk.

Note: You can mix a high risk asset with a low risk asset to get a similar asset of moderate risk. However, this is not always the case and is often difficult to assess exactly the level of risk, especially for high risk assets. It’s therefore much better to get a moderate risk asset if you want a moderate risk. If you are looking at this in the context of a portfolio you should also look at Asset Allocation.

Creating a Diversified Asset Allocated Portfolio

Here are a few guidelines when trying to create your portfolio:

Cash: Keep enough cash on hand for daily purchases and small emergencies. It can be wise to keep enough money in your bank account to avoid the fees.

Gold: Many investors keep a small amount of physical gold and cash on hand. This can be useful in financial crises like the great depression where limits are imposed on the amount of money that can be withdrawn. Gold is also extremely safe and not tied to a countries currency.

Property: Your house is an investment as it has value and should be considered as such.

Bonds: They are generally not good investments unless you are trying to protect what you already have. This was not always true however and is dependent on the interest rates.

Stocks: Diversification of stocks is important and generally the cheapest way to do is with mutual funds or exchange traded funds (ETF). Growth Stocks are generally considered to be riskier than income stocks.

Examples

Here are examples of asset classes we might assign to each investor. Note: Asset allocation is not an exact science and can have big differences between one opinion and the next.

Low Risk Portfolio: Retiree with high investment knowledge, very low income and moderate risk aversion. Moderate Risk Portfolio: Middle aged investor with low income, high investment knowledge and moderate risk aversion with large savings. High Risk Portfolio: Young investor with good income and high investment knowledge and low risk aversion and high spending with no owned property.

Berkshire Hathaway and 3G capital took control of Kraft foods and Heinz ketchup not long ago, where efforts first focused on Heinz.

After replacing most of the top-level management (and many of the juniors), Heinz also shaved thousands of jobs in an effort to cut costs. The efforts seem to have worked; it boasted some of the best margins in the food industry after the cuts were implemented.

Hathaway and 3G are now turning their sights on Kraft, and hoping many of the same policies will work. In addition to job cuts and management replacement, they will be moving the corporate headquarters from the Suburbs to downtown Chicago, placing strict limits on travel and food expenses, and even removing free snack refridgerators from staff break rooms. Employees will also no longer be allowed to bring competetor products to the office for lunch, as it “voliates the respect for the food we make”, among other restrictions.

Only time will tell if the belt-tightening will pay off!

Everyone paying attention to the news lately knows that there has been a lot of rough water over the last month or so; Gold and Oil have been tanking farther than usual, the Chinese currency devaluation rocked global markets while the Chinese stock market plummetted.

Which is, coincidentally, a great time to start looking at what to buy. For investors that have been sitting on the sidelines, the classic adage “buy low, sell high” is becoming more true than ever; when markets have bottomed out is the best time to start scooping up cheap assets. These assets are now cheap for a reason; the risk associated with them, but investment firms playing the “long game”, looking out 3 or more years into the future, are starting to see opportunity. Stocks like Micron Technology (MU) have lost more than half their value, but their actual business case is not worth half what it was a year ago.

For the long-sighted investor, this might be a time of great opportunity!

An asset is anything that has monetary value and can be sold. Assets can be anything from a pencil (though it is not worth much) to a skyscraper to things like Stocks and ETFs.

There can also be intangible assets such as the value of a brand name or logo.

Details:

Assets generally refer to either something that you intend to sell later for a profit, or something you are actively using to make money. This means that assets generally fall into two categories, Investments and Capital. The easiest way to tell them apart is this:

If you are using it to build something or make something (like a computer or a factory machine) that you later sell, it would be capital

If the value of the asset is the asset itself (like stock, bonds, or gold), it would be an investment

There are also some things that fall in the middle: For example, your house is considered an “investment” even though you are using it to live in, because hopefully it can one day be sold for a profit, with that profit being likely used for retirement.

Note: Typically when asset is mentioned in a financial context, it usually refers to real estate, precious metals, investments such as stocks and bonds, cash and other financial devices.