Have you ever wanted to start a business? Maybe you want to know the difference between a lemonade stand and Minute-Maid, besides just the size of the companies.

Different types of companies have different levels of liability (meaning level of responsibility) for the owner or owners. What this means is that the more liability an owner has, the more that owner is responsible for the company’s debts. Different types of businesses also have different rules on how they can be managed, and how the owners can be paid.

Sole Proprietorship

This is the simplest type of business – the entire business is owned by one person. There generally are no requirements to operate a sole proprietorship – if you ever sold something, you have already worked as a sole proprietor.

Sole proprietorships can have many employees, but the key factor is that the business itself is owned by just one person.

Ownership Liability

In a sole proprietorship, the owner takes the full liability for the entire company’s debt. That means that if, for example, the owner took out a loan to start the business but then goes bankrupt, he or she could have their other assets seized by creditors (such as their car or home).

This also means that if someone wants to sue the business, they can also just sue the owner directly (even if the business has already closed).

Most larger businesses don’t want to always have that much liability, so usually as businesses get larger, then tend to move on from sole proprietorships into other business types.

Owner Compensation

With a sole proprietorship, everything that is owned by the company is owned directly by its owner. This means that most owners can (and usually do) mix their personal finances and business finances. An example of this would be taking money directly from your cash register to buy your personal groceries.

This means that the owner keeps 100% of the profit from the business for him or her self, and reports all the income, profit, and loss on their own personal taxes.

“Doing Business As”

A sole proprietor may still want to register a company name (although this is optional), which they can then use for bank accounts and legal paperwork. This is known as “doing business as” another name, and the rules vary by state. In this case, the sole proprietor still has unlimited liability, but can use another name for their business.

Partnerships

“Partnerships” exist when two or more people decide to run a business together. There are “General Partnerships” and “Limited Partnerships”.

Unlike a sole proprietorship, a partnership requires a contract in order to exist, where the partners establish the existence of the partnership. Like a sole proprietorship, the owners still own the entire company themselves, along with all its profits (and losses), but the partners can choose to use a “Doing Business As” name.

General Partnerships

With a general partnership, the business works just like a sole proprietorship, but with several owners instead of just one.

Ownership Liability

All of the partners are fully liable for the entire business, just like a sole proprietorship. Partners are also liable for the actions of their other partners any time one of them is acting on behalf of the business.

For example, if you have a partnership that sells stereos, and your partner agrees to sell them at $1 each, you are obligated to honor that agreement.

Ownership Compensation

All of the profits and losses are divided equally between the partners (although in the initial contract, the partners can specify that one gets a greater share than the others).

Limited Partnerships

With a “Limited” partnership, there is at least one general partner, plus at least one “Limited Partner”. The limited partner does not have all the rights, responsibilities, and obligations as the general partner, but also does not share the full liability either.

Ownership Liability

The general partner has the same liability has the same rights as a general partnership, but the limited partner has somewhat less (usually only as much as they invested in the company to start with). This also means that the general partner might not be liable for the agreements made by the limited partner, if he or she can show that those actions were “negligent” or purposely harmful.

Ownership Compensation

The limited owner usually has their compensation set to the same restrictions as their liability – there might be a cap to how much they can “take out” of the business. The specific rules depend on the terms in the partnership contract.

Corporations

The biggest type of business is a corporation. These operate under different rules from sole proprietorships and partnerships – a Corporation is its own legal entity (meaning it can have its own bank accounts, and be sued directly). Corporation’s most useful feature (as far as the owners are concerned) is totally limited liability, but this comes at a high cost of management and organization.

Ownership

When a corporation is created, it exists with a certain number of shares of stock. Whoever holds those shares is a part owner in the company – how much they own is based on how many shares they hold.

Instead of the company being managed directly by the owners (like a sole proprietorship or partnership), the shareholders then elect a “Board of Directors”. The day-to-day management of the company is overseen by the Board, but for some larger decisions there are occasionally calls for each stockholder to vote. The Board of Directors is also responsible for hiring and firing the highest levels of management (like the CEO), and the Board is the direct “boss” of those managers.

Ownership Liability

The owners of the company (stockholders) have entirely “limited” liability – they can only lose as much as their stock is worth. This means that if a Corporation goes bankrupt, the individual stockholders will lose the entire value of their stock, but nothing more.

A “Contract” is a legally binding agreement between two parties (people, companies, or both). Having a contract means that if one party does not keep their word, the other can sue them in court to either force them to fulfill their side of the agreement, or pay back compensation.

What Makes A Contract Binding?

Not every agreement is a binding contract, but every contract has a few necessary parts.

Consideration

[rich]If you have ever seen a news article about a CEO who has a $1 salary, it is because of Consideration. He or she would not have an employment contract if the company did not have to give up something![/rich]”Consideration” means both parties have something required of them, something they would not normally be doing except as part of the agreement. If one party is agreeing to do something but the other party does not need to do something else in exchange, it would be considered a gift and not a contract.

Offer and Acceptance

The “Offer” is what each party says they will do. The offer needs to be very clearly defined to make sure both sides know exactly what they are agreeing to do, and what they are getting in return. The “Acceptance” means that both parties agreed to take each other’s offer. If you do not have a very clearly defined offer, you do not yet have a contract. Likewise, if both parties have not yet fully agreed to the offers, they do not yet have a contract.

For example, if Alice owns 10 shares of Google [hq]GOOG[/hq] stock and offers to sell some of her shares to Bob, and Bob agrees that he will buy them. They do not yet have a contract. This is because the Offer was not yet clearly defined – the agreement does not include how many shares, at what price, or when Bob would receive them.

Now let us say that Alice comes back and says she will sell 5 shares of Google [hq]GOOG[/hq] at $700 each to Bob, and he will get them next Monday morning. In this case, we still don’t have a contract yet. Bob agreed that he wanted to buy some shares, but he did not yet agree to this specific offer of 5 shares at $700 each next Monday, so we do not yet have an agreement.

Intention To Make A Legal Contract

Both parties need to actually intend to make a legally-binding contract. This might seem obvious, but this is the key difference between an informal agreement and a binding contract. For example, you might have an agreement where you mow your neighbor’s law for $10 a week. There is a clear offer and clear acceptance, but since the consideration is so low for both parties, it may not be clear that both parties intended the contract to be legally binding – just an informal agreement.

What Can Void A Contract?

If you have your Consideration, Offer, Acceptance, and Intent, you might still not have a contract because of a few factors that can break them.

Legal Capacity

“Legal Capacity” means that all parties need to be able to make a contract to begin with. There are a few ways someone might be considered to not have the legal capacity to enter a contract:

Anyone under the age of 18

Someone who went bankrupt in the last 5 years buying something worth more than $6,000 (without telling the other party they went bankrupt)

Anyone with a significant mental disability

There exceptions to these exceptions too – someone under the age of 18 can still enter a binding contract for a “necessity” (like food or shelter), but not for most other things.

Forced Agreement

All contracts must be entered in “Free Will”, meaning you can’ force someone to enter into a legally-binding contract (so the mafia can’t force you into a contract by threat, for example).

Illegal Contracts

Even if you have everything else, your contract might still not be valid because it is asking something illegal. For example, you can’t have a legally-binding contract to sell illegal drugs.

Does A Contract Need To Be In Writing?

It depends! Generally speaking, verbal contracts are a lot harder to prove they have all the necessary elements, but if you have witnesses, it might still be legally enforceable. Some contracts, such as land sales, do need to be in writing.

If you want to make sure you have a legal contract, you should always get it in writing.

The most widely traded financial asset in the world is not any particular stock, oil or gold – it is the EURUSD (Euro/ US dollar) currency pair. The pair represents two of the largest economies of the world. Created to facilitate cross-border trading among European and American partners, the euro (EUR) has risen to become the second largest currency in circulation after the US dollar (USD). As the official currency for 16 countries that comprise the Eurozone, the euro has also become the second largest reserve held currency in the world after, again, the US dollar. The US dollar itself needs no introduction. It is the official currency of the world’s largest economy and is generally accepted as the reserve currency of the world. Most global central banks hold a big part of their foreign currency reserves in US dollars while many other countries peg the value of their currency to that of the USD. Additionally, the OPEC (Organization of the Petroleum Exporting Countries), the world’s largest producers of oil, transacts in US dollars. There is a phrase in the financial markets that goes ‘The Dollar is King’ and it is easy to see why.

The EURUSD currency pair is incredibly popular among traders. But should you trade the pair that represents two of the economic world’s most powerful trading blocs?

Liquidity

In the financial markets, liquidity is the ability to sell out of an investment without triggering a significant movement in price. A liquid asset is easy to cash up because there are many able and willing takers. An illiquid asset, on the other hand, is difficult to sell out without suffering a price hit. The EURUSD is the most liquid financial asset in the world and enjoys a very high liquidity premium. Approximately 80% of the world’s transactions are completed in either of these two currencies. As the most liquid asset, investors receive transparent EURUSD quotes throughout the day because its price cannot be influenced by few market players, as is the case with other assets such as stocks. Liquid assets also tend to make regular price movements unlike illiquid assets that are prone to occasional price whipsaws.

Assets with massive liquidity also have the benefit of low transaction costs. On most online trading platforms, the spread or commission for trading the EURUSD ranges from zero to a few hundredths of a cent. While it is not any easier to trade liquid assets than illiquid ones, it is definitely less risky.

Volatility

Volatility refers to the frequency and severity of an asset’s price movement. Volatile assets move faster and make bigger trading ranges in any particular trading session than the less volatile assets. In markets such as binary options, where investors trade on the direction of the price movement of assets, volatile assets offer more profit opportunities than the less volatile ones. The EURUSD almost always guarantees volatility at all times due to the many factors that impact on its price and can offer great trading opportunities for investors.

Trading on Fundamentals

The EURUSD offers investors the easiest way to profit using fundamentals or fundamental analysis. The euro itself is sensitive to political and economic developments in the 16 countries it represents. The number of nations that release data that might impact on the euro means that there will always be numerous opportunities to profit on a daily basis. Add that to news coming from the US and its major trading partners, and it is almost mandatory to include this currency pair on your asset watch list.

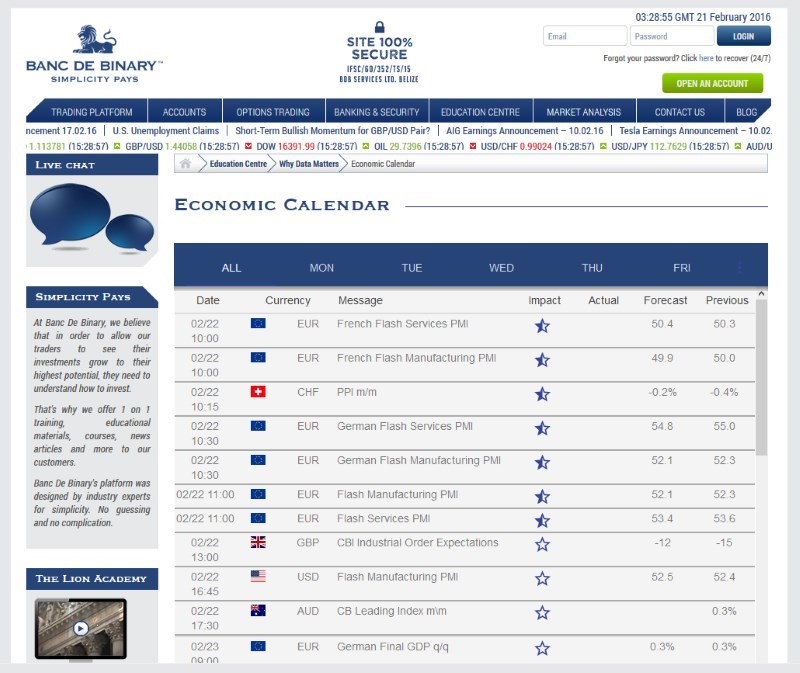

Not all news is traded though. Investors mostly trade new releases that are likely to have a high impact on the price value of the EURUSD. Such news includes, for example, the US Nonfarm Payrolls and the Eurozone CPI (consumer price index). Investors can track such economic news conveniently using a binary options app or site that contains the Economic Calendar tool.

EURUSD Current Fundamental Analysis

The EURUSD currency pair has lately been driven by market sentiment. After drifting higher since the start of the year and into the first week of February, after the non-committal sentiments from the US Federal Reserve, the pair has now closed lower for 5 consecutive days. The recent publication of the European Central Bank (ECB) January meeting eased the downward pressure on the pair. In the meeting, ECB’s head Mario Draghi discussed about further downside risks and vowed action in March. In a symbol of unity, Draghi’s most vocal opponent Jens Weidmann provided his support for the quantitative easing program. Of late, though, the euro has acquired a safe haven status and continues to ignore many pieces of negative data coming from the Eurozone. This general mood for the euro is upbeat with crude oil prices also rising as well as the increasing market expectation that the ECB will do something next month.

The dollar, on the other hand, is affected by a cautious and uncertain Fed. Strings of positive data are coming out of the US, the latest being a fall in unemployment claims to 262K against expectations of 282K, but the greenback is not reacting accordingly. The main reason has been recent commentary from Fed officials, including its chair Janet Yellen, which have not given a clear direction on the future of interest rates in the country. As it stands, the markets now anticipate a rate cut more than a rate hike. With crude oil prices seemingly starting to rise, pressure on the dollar could increase.

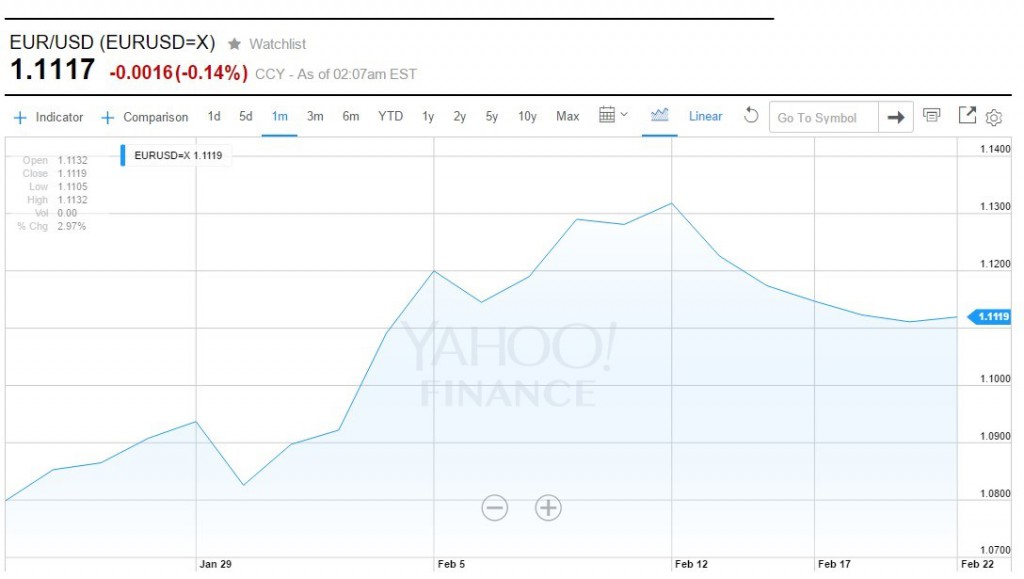

EURUSD Technical Analysis

The current price of the EURUSD is 1.1170. The pair seems to have found support after retreating lower for five straight days. The pair has largely been trending this year before breaking above its 200-day moving average at 1.1105 this month and going on to form this year’s current high at 1.1375. It fell from those highs and found support at 1.1085 (21-day moving average). The pair is now back and hovering above its 200-day moving average, which is expected to provide support for the medium term. Important technical support levels to watch out for in the near term are 1.1080, 1.1045 and 1.1000. The resistance levels to watch out for are 1.1160, 1.1200 and 1.1245.

Final Word

In the medium term, the EURUSD is expected to be driven by market sentiment. The market has shown contempt towards the Federal Reserve and the dollar, while it seems to cheer on the euro. Upcoming fundamental data could prove crucial for the pair in the medium term. Positive news for the euro could send the pair higher as will negative news for the dollar. Negative news for the euro could be ignored by the market or it might send the pair marginally lower, same as positive news for the US dollar. All in all, with numerous economic news affecting the pair scheduled to be released in the coming days, investors should look to exploit the amazing and lucrative opportunities the EURUSD will offer them.

Our April Trading Contest is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest!

Click Here To Join The Next Contest!

April Stock Market Contest

Stock Trading Contest Result

TJack43

EddieB18

Housemanager

brucehaan

wolforda17

See The Trading Strategies From This Contest!

Janene’s March Trading Strategy-Contest: March Trading Contest Final Portfolio Value: $131,022.78 Trading Strategy For This Contest I’ve watched the market as it fluctuates, learning to buy and short gold as it adjusts. I tend to go with my gut instinct when buying stocks. Sometimes it works, sometimes, not so much. The best thing you can do, to help you Read More...

Vicky’s March Trading Strategy-Contest: March Trading Strategy Final Portfolio Value: $101,169.24 Trading Strategy For This Contest Trading Strategy: Investing for the first time in the stock market is very overwhelming; even if it is done with virtual money. I’ll start saying that implementing a strategy takes a lot of practice and patience. You must begin understanding some of Read More...

About The Challenge

We held trading contest from March 8 through March 31, 2016, with over 4,000 traders joining in! We gave prizes to the top 5 finishers. This was the third prized contest of 2016!

Prizes

Top 5 Finishers Each Win $100

Rules

There will be a full audit at the end of the investing contest on all winners to verify any corrections due to stock splits, dividends, or any other corporate action our team may have missed. Only legitimate portfolio returns will be counted in the ranking.

Each person is allowed only 1 entry. Users with multiple portfolios in the contest will be disqualified.

The usernames of the winners will be made public, but not their actual first name, last name, nor email address.

No member of the HowTheMarketWorks Team is eligible for any prizes

Other Prized Contest Results

Fall 2017 Challenge-Win prizes in our stock market contests! Find all of the information for any stock contests with prizes we are currently running here! You can also find information on past contests and their winners. Register Here To HTMW Fall Challenge Who can join? Anyone can join! Joining our stock market contests is completely free, so Sign Up Read More...

Back To School Challenge-Our Back To School Challenge is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! Stock Trading Contest Result Fractals7 Namburiv Catspaws Igorski123 Read More...

April Trading Contest-Our April Trading Contest is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! Stock Trading Contest Result TJack43 EddieB18 Housemanager brucehaan wolforda17 About Read More...

March Trading Contest-Our March Trading Contest is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! Stock Trading Contest Results MichaelGebhart +53.77% wpeldiak +50.55% Janene +31.00% Read More...

February Trading Contest-Our February Trading Contest is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! Stock Trading Contest Results almater1 +44.59% Housemanager +43.9% Michael +35.1%% Read More...

January Stock Trading Contest-Our January stock trading contest is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! Stock Trading Contest Results smithjj5 +30.19% blowke +28.64% qtran12203 Read More...

December Stock Trading Contest-Our December stock trading contest is now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! Stock Trading Contest Results smithjjj5 – +36.28% Return mchung37 Read More...

November Investing Contest Results-Our November investing contests are now finished, we had tens of thousands of trades placed to fight for the top spots! See the winners below! If you want a shot at a cash prize yourself, join our next contest! Click Here To Join The Next Contest! First Weekly Contest blowke +15.56% Second Weekly Contest brendanriley +15.41% Read More...

October Stock Contest Results!-The October stock contests are finished, with over a thousand participants from all over the world! We had hundreds of thousands of trades placed, and already gave away almost $1000! See who won below! First Weekly Contest The Top 5 performers by portfolio value were: hoabidebay +16.94% kingsalman+14.36% brucehaan +14.08% daniellopez +10.16% Housemanager +9.83% The Read More...

September Monthly Million Challenge!-The September Monthly Million Challenge is the first in our Monthly Million series, with over a thousand participants from all over the world! The rankings were fierce, with the HowTheMarketWorks team scattered throughout, but you’ll be surprised who won! The Top 5 performers by portfolio value were: AngelRivera +30.81% Janene+23.14% wkaraman14 +18.15% puttno2 +12.63% smithjjj5 Read More...

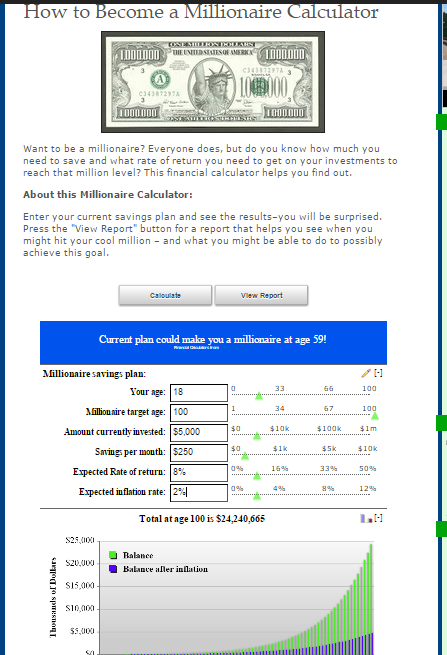

Knowing your net worth is the first step towards growing it! This tool will help you organize your assets in one place, and even help project how they will grow in the future.

If you have used our Home Budget Calculator to help see where you can improve your savings, the next step is measuring your net worth to see how to make it grow.

Once you have found your net worth, you can use our Saving to be a Millionaire Calculator to see what rate of return you need to reach to hit your savings goals!

I’ve watched the market as it fluctuates, learning to buy and short gold as it adjusts. I tend to go with my gut instinct when buying stocks. Sometimes it works, sometimes, not so much. The best thing you can do, to help you succeed in the market, is homework. I also buy the cheaper stocks as they fluctuate more rapidly than do the expensive ones.

It is no longer news that oil prices have been crashing in the last couple of months towards the end of 2015. In fact, in the last one year, the West Texas Intermediate is down 15.6% and the Brent Crude is down a massive 28.8%. The crash in oil prices is good news for most folks and news headlines coming out of the energy market is likely to gladden the heart of businesses that have oil as a major expense.

Airlines, utility companies, refineries, and manufacturing plants would have surely recorded a marked drop in their expenses as oil prices continue to stay depressed. Individuals have also benefited from the drop in global oil prices because the weakness in crude oil has slashed gas prices towards record lows. Airline prices are being slashed and shipping costs have also been reduced.

Oil is on a rollercoaster ride

At the start of this year, it seemed that oil prices would improve after oil enjoyed a series of false starts that raised the hopes of a rally in global energy prices. For instance, the West Texas Intermediate crude is up 2.07% in the year-to-date period and the Brent Crude is up 6.58% since the markets opened for trading this year.

Investors and traders who know how to trade crude oil understand that the key factor that affects the trading price of crude oil is the dynamics of demand and supply. It doesn’t matter that you are interested in the WTI or the Brent Crude oil, the back and forth between the forces of demand and supply often determines the trading price of crude oil on the global market.

One might argue that other factors apart from the dynamics of demand and supply can affect oil prices –and you’ll be mostly right. Geopolitical concerns might affect the price of crude oil, acts of terrorism, natural disasters, and economic policies might also affect the price of crude oil. However, the underlying truth is that the aforementioned factors might lead to an increase/decrease in the demand or supply of crude oil. When the demand for crude oil exceeds its supply, the price will rise and when the supply of crude oil exceeds its demand, the price will fall.

Iran dashes hopes of a rally in oil

Any hopes that crude oil will see a rally any time soon has been dashed again as Iran moves to sabotage a potential deal to cut global oil supply. On Monday, Iran indicated that it won’t cooperate with plans by oil producing countries to find a way to slash the supply of oil in order to jumpstart an increase in the price of crude oil.

Saudi Arabia and Russia have been spearheading a move by OPEC and non-OPEC countries to find a way to reduce their oil production output in order to end the supply glut that has been exerting downward pressure on oil. However, Iran’s oil minister, Bijan Zanganeh noted revealed that Iran won’t consider reducing its oil production output until its current oil production levels rises to 4 million barrels per day. Iran currently produces about 3.3 million barrels of oil per day and the country plans to increase production by 500,000 barrels per day this year.

Iran was producing about 4 million barrels per day before the United Nations imposed sanctions on the country in 2012 because of its nuclear program. Analysts have also noted that Iran faces an uphill task in its target to increase oil production by 500,000 bpd in 2016. Tamas Varga, oil analyst at London brokerage PVM Oil Associates says, “Oil is down because Iran said they would only join the output freeze group once they reached production of 4 million barrels a day (bpd)”.

Oil futures traders win either way

Trading crude oil futures is a smart way for traders and investors to profit from the global energy market irrespective of whether oil trades upward, downwards or sideways. The fact that Iran is practically throwing its foot down against any deal to cut crude oil supply indicates that oil prices might not be heading up any time soon. It is a well-known fact on Wall Street that oil CFDs are very volatile but Iran’s current actions makes it somewhat easy to predict where oil prices are headed.

Analysts at Morgan Stanley agree that oil prices have a steep drop and that oil prices are not likely to fall much lower. However, they are not confident that oil will see a decent rally anytime soon. In the words of Morgan Stanley analysts, “Oil prices now seem to have bottomed, even though they are likely to stay subdued for the rest of this year before starting to move higher in 2017.”

When talking about Banking, people generally group Banks, Credit Unions, and Savings & Loan companies all in one group. They do provide similar services, but they each have specific differences that might make them a better or worse fit for your financial needs.

What They Have In Common

All three of these institutions can do all the things you would normally associate with a “bank” – opening checking and savings accounts, making commercial loans, and issuing residential mortgages.

Savings and Checking Accounts

When you deposit cash at a bank, credit union, or savings and loan, you will put it into a checking (also called “Current”) account or a savings account.

Savings Account

Savings accounts are usually the first type of bank account you might open as a child. This is an account where you can make deposits of cash, and earn interest. How much interest you earn can vary a lot based on how much you have saved, how often you withdraw, the overall market interest rates, and even just by institution.

Savings accounts pay interest because banks use the money you have saved to make loans to other people and businesses. This is also the reason that you might get a better savings rate if you keep the balance in your account higher – if the bank knows that your deposit isn’t going to suddenly be withdrawn, they are more secure in lending it out and so encourage you to keep it saved. If you tend to withdraw a lot of your money from a savings account frequently, the bank has a harder time maintaining that cash balance necessary to make loans, so they are not going to give as high a rate. Credit Unions generally specialize in savings accounts.

Checking Accounts

Checking accounts are where you store your “day to day” money, meaning you will have a lot of frequent deposits and withdraws. Your checking account is the account that gets drawn down when you write checks, use a debit card, and usually where you pull money from when you use an ATM.

Since banks have a lot more management necessary for a checking account (processing check payments, keeping many detailed transaction records, ect), there are usually fees associated with owning a checking account, and it does not usually pay interest. Some institutions might cancel your fees if you keep a minimum balance in your checking account (just like they give higher interest rates if you keep a minimum balance in your savings account), but this can vary widely by institution.

Making Commercial Loans

A “Commercial Loan” is a loan made to a business, usually to “start up” or to expand their operations. Banks, Savings and Loans, and Credit Unions differ a lot on how much of their business comes from commercial loans, but for small businesses looking to secure start-up loans, each institution might be a good choice.

[rich]Just because banks specialize on commercial loans does not mean they offer the best rates for you! If you want to start a business, always explore all your alternatives and shop around for the best interest rates![/rich] Commercial loans have a lot of different types, from a commercial mortgage (to buy new land or build a new building) to just the costs of renting and renovating a storefront and getting open for business. The duration of these loans can be anywhere from 18 months (small, short-term start-up loans) to 25 years (larger commercial mortgages). Unlike a normal mortgage, it is rare for a business to pay off their entire loan. When a business pays off a certain percentage of its loans and has continued to grow, they will usually use the equity they have built up to make more loans to finance their continued growth. This does not apply to some small businesses without a large expansion strategy, but does apply to medium and large-sized businesses. Banks generally specialize in commercial loans.

Residential Mortgages

A residential mortgage is a loan that a person or couple takes from a bank, credit union, or savings and loan institution to buy a house. A residential mortgage is usually for a very large amount (usually over $100,000 and often more than $1 million), and is usually paid over 25-30 years. Residential mortgages are for very large amounts of money and take a very long time to pay off. This means that the institution you borrow from for your mortgage needs to have a lot of deposits available to make sure they have enough cash to make these loans. Savings and Loan institutions generally specialize in Residential Mortgages.

What is the difference between Banks, Credit Unions, and Savings and Loans?

Despite offering some similar services, there can be huge differences between these three types of financial institutions.

Banks

Commercial bank branch. Photo by Mike Mozart

Banks are for-profit corporations with a charter issued at the local, state, or national level. They issue stock which is owned by investors, and those investors elect a board of directors who oversee the bank’s operations. Banks generally specialize in commercial loans – making loans to businesses to help them get started or expand.

Local banks are becoming less common, while national banks are becoming a lot more common. Over the last two decades, many local banks have been bought or merged with State banks, who in turn were bought or merged with National Banks. This has some advantages – by using a national bank, you will have access to a bank branch, ATMs, and in-person account services in a lot more locations than smaller institutions. Larger banks generally offer a lot more account management services and account types than other institutions. For example, a national bank might offer some types of checking accounts that offer points and rewards for certain types of purchases (like gas and groceries).

Because they are much larger, banks also generally have better online banking services, with more account management services. This includes things like transferring between your checking and savings accounts, viewing the checks you have previously written, checking balances with mobile apps, opening and closing credit cards, and managing automatic payments and deposits. Banks will also generally offer a lot more choice for residential loans as well.

There are some significant drawbacks as well. Banks generally have higher fees than other institutions for its services, with lower interest rates for savings (although this is not always the case). It is fairly rare to find truly “free” checking accounts at banks. The large amount of choice you have for your savings and checking accounts can be a drawback as well – if your life circumstances change from what they were when you first opened your account, you might end up with more fees and less benefits than with a different account type, but very few people consider changing very often.

Credit Unions

Credit Union, photo by Mike Mozart

Credit Unions are the financial opposite of banks – they are non-profit, almost exclusively local, and are owned by the people who make deposits. Every member who makes a deposit at a credit union is a part-owner, and can vote on issues relating to the union. They can also get elected to be the managers of the savings and loan.

Credit unions specialize in savings accounts and making short-term loans. Since they are non-profit, all the profits made by these loans are given back to the credit union’s depositors as dividends. Many depositors also prefer credit unions because of the more “Personal Banking”. This is because credit unions are almost exclusively local, and the credit union relies on the deposits to stay in business, and so they often have a reputation for excellent customer service. Since they are smaller with less management costs, Credit Unions will often have better savings account rates than a bank, and you are more likely to find free checking accounts.

[rich]Just because credit unions do not specialize in commercial loans and residential mortgages does not mean they don’t make them! They might not have as many options available as a bank, but you might find a better interest rate![/rich]Credit Unions also have their own drawbacks. They do not focus on commercial loans, and so if you want to start or expand a business, you might have to look elsewhere. They also prefer short-term loans, so you might also not be able to get many options for a residential mortgage. They are also much smaller than banks, which means you might not have access to as much of the online account management features, like bill payment and opening new accounts. If you travel a lot or move, the local credit union will also not be able to provide much service if you are outside their immediate area.

Savings and Loans

Savings and Loan. Photo by the Boston Public Library

Savings and Loan institutions focus strongly on residential mortgages. In fact, by law they need to invest 65% of their assets in residential mortgages, and only up to 20% in commercial loans. They can also be local or national (like a bank).

Savings and Loans can be organized like a bank (owned by investor shareholders) or a credit union (owned by the depositors), but is always for-profit. Specializing in residential mortgages means that you might find the most flexibility for your mortgage at a Savings and Loan, and their smaller focus means that you will often see better terms for mortgages here than elsewhere (but not always!).

Savings and Loans do suffer from some of the same problems as credit unions. Their emphasis on slow-maturing mortgages means they are often lagging behind banks with account management and online services.

In the last six months we have witnessed strong volatility in the global currency markets. Emerging markets currencies weakened aggressively against the U.S. dollar, which has strengthened substantially leading up to the Federal Reserve’s U.S. benchmark interest rate hike in December of last year. Volatility in the currency markets is not just an issue for governments and investors, but also for companies involved in international business.

Currency Risk Affects International Businesses

If you are a business that has operations outside of your country’ borders you will inevitably have to deal with currency risk. Currency risk, also known as foreign exchange risk, refers to the risk of a potential loss stemming from exposure to fluctuations in currency exchange rates. For example, if you are a U.S. based company and you have revenue-generating operations in the United Kingdom you will generate revenue in British pounds that will need to be transferred back into dollars. If, for example, your revenue in Q1 from your company’s U.K. business was GBP 10 million, but the pound weakened 5% against the dollar in Q1, then your actual revenue will be worth 5% less, as soon as you exchange it back into dollars at the end of Q1. Hence, it is so important to implement an adequate currency risk hedging strategy, using financial derivatives, when you have operations overseas. Having said that, it is not always easy to use the full range of possible hedging tools. Retail clients and SME’s, for example, have limited access to these options via banks. However, they have the option to use commercial FX services instead. Banks, on the other hand, tend to only provide currency-hedging solutions to large multinational corporations. A cfd online trading brokerage firm can provide access to all major world markets with FX trading solutions best suited to your needs irrespective of whether you run a freelance business, SME, or large corporation.

FX Forwards

There are several possible financial derivatives used in the currency market that can help corporations, SME’s and retail clients hedge their foreign currency exposure. The most commonly used derivatives in this space are so-called FX forwards. An FX forward contract is an agreement between two parties to buy or sell an amount of a foreign currency at a specific price for settlement at a predetermined future date. Using FX forwards you can ‘lock in’ the exchange rate at which you will exchange your money at the date you are required to transfer it into another currency. This hedges you entirely against currency fluctuations. However, it does not let you benefit from a beneficial move in the foreign currency that you are generating revenue in. This is the only downside of using FX forwards as your currency-hedging tool of choice.

FX Options

An alternative to FX forwards would be the use of FX options to hedge your currency exposure. Through purchasing a FX option you have the right but not the obligation to exchange an amount of money denominated in one currency into another currency at a pre-determined exchange rate on a specific date. The benefit using FX options over FX forwards is that if the foreign currency strengthens, you can still benefit fully from this move (minus the premium for the FX option), as you do not have the obligation to exercise the option. So, if you know that if the foreign currency hits a certain level your foreign business will lose revenue, you can purchase a FX option with a strike at that level. You can exercise the option once that level has been reached to hedge out your currency exposure in that currency.

Participating Forwards

A third way if how you could hedge your currency risk is by using so-called participating forwards. Participating forwards provide a guaranteed FX rate for your currency exposure, while still allowing you to benefit from beneficial exchange rate moves on a predetermined portion of your FX exposure. For example, if you need to exchange GBP 1 million in three months time into U.S. dollars, you could enter into a participating forward contract that allows you to exchange the full amount at GBUSD 1.40 and agree a participation rate of 50%. Should the currency strengthen, however, to say 1.50, then the participation forward will allow you to exchange GBP 500,000 at 1.40 and the remaining GBP 500,000 at the prevailing spot rate of 1.50. This is an excellent way to hedge currency risk exposure as you are not required to pay a premium for this derivative transaction.

Financial Records are what you use to have an easy way to tell where all your money and assets are, and exactly how much you have, at any given time.

They are not one document, or even one type of document. In fact, most people’s financial records will not look the same as anyone else’s, because each person has unique ways of organizing their information to make it most accessible for him- or herself.

Financial Record Basics

Your financial records are useful for many reasons, but they generally fall into two categories. First, they make it much easier to do financial planning (particularly managing your saving and investing). Second, they can be extremely important (often legally required) for tax purposes.

Financial Planning

[rich]When you set a savings goal, make a plan for how you intend to save it. If you get money another way, like a gift, don’t count it towards that savings goal, or you might have a hard time picking achievable goals later. [/rich]When you are building or evolving your financial plans and setting new financial goals, you need to start with accurate financial records so you know exactly where you are starting from, and know exactly when you have reached your goals. For example, if you want to save $300 over the next 4 months, you need to know how much money you have now, and in 3 months you will need to be able to make the same measurements.

If your current bank balance is $250 and you want to save up to reach $400, your savings goal would be to earn extra cash or trim your savings to reach it. If, however, you find an uncashed check for $150 from your last birthday in a pile of papers on your desk and deposit it into your account, you will hit that $400 target without actually accomplishing anything. This is one example of poor financial records hindering your ability to set and reach your targets.

Taxes

Pictured: the money you can’t get back because you didn’t save your receipt

The government uses taxes and tax returns to try to encourage or discourage certain behavior, or to make some expenses more “fair”. For example, if you buy a car, you can usually get a partial return for the sales tax based on the vehicle’s value, how environmentally-friendly it is, or how much you use your car while at work as part of your job.

This means that if you want to claim these tax returns, you need to have accurate documents on how and when you bought it, and odometer readings showing a very close estimates of how much you use your car for work. Without these documents, you can’t claim the tax returns, and can end up missing out on a lot of money.

Types of Financial Records

There are dozens of types of records, but the key is keeping them all organized. You can divide all your records into two big buckets – “Primary” records (which will be extremely varied and scattered), and “Secondary” records (which you will generally maintain yourself to keep your primary records organized).

Primary Records

Receipts

[rich]Even if you plan on always doing your taxes yourself, everyone should meet with a financial planner or tax adviser occasionally to discuss tax incentives they might be eligible for. This will make it a lot easier to know which receipts are worth savings![/rich] If you want to claim any tax breaks, you will need to keep careful track of your receipts. These are the most basic financial record there is, just a piece of paper showing that a transaction has taken place.

Depending on where you live, you should always save the receipts for large purchases (like your car’s bill of sale). Many cities also provide tax breaks if you use public transit, so it is also a good idea to save those receipts.

They are also useful to keep beyond your taxes. For example, utility bills and receipts are often required as a “proof of address” when you want to open a bank account. If you get in a conflict at a later date over a bill being paid, having a receipt can shut down the problem immediately, while proving otherwise can be a long and drawn-out process.

Bank Records

Your bank account will be one of your most important sources for financial records. Usually, your entire transaction history is saved for a few years (including every check you write), along with your current account balances. If you do not have a receipt for a payment (for example, if you write a rent check every month), you can still have a record of that transaction in your bank account.

You will have different records available based on different account types. For example, if you have a savings account, you might have more records on deposit amounts and dates, with accumulated compound interest. If you have a checking (or “Current”) account, you will have your current available balances, along with your transaction history of your checks, debit card transactions, and ATM withdrawals. Your bank records will be an invaluable resource when you are building and changing your Spending Plan.

Income Reports

Your income reports are statements showing how much money you’ve earned, usually along with how much income tax and social security you have paid, in a given year. The most common of these is the W-2 form in the United States, but you might have others if you are self-employed or work occasional odd jobs on the side. These are necessary to file your taxes, but are also useful to see how your income evolves over time.

Investment Statements

If you have any stocks, bonds, or other investments, you will also get regular account statements from your broker. This will include your cash balances (available for withdraw or purchasing more securities), the total net market value of your portfolio, the amount of any dividends you have received, the total expenses of your investments (this is most important with mutual funds). Your investment statements are essential for tax purposes. Unlike claiming deductions for receipts, you are legally required to report any investment income you receive, so having ready access to these documents will be essential.

Personal Property Inventory

[rich]Not everything you own belongs on this inventory! Only include bigger items that have decent resale value, this will keep your list smaller and easier to maintain in the long run. [/rich]Unlike the other primary records, this is one you will make and maintain yourself. Your personal property inventory is basically a list of what you own, where it is located, and its estimated value. This seems fairly simple when you are still in school, but there are more than a few cases of large amounts of cash stashed and forgotten. Also unlike the other records, your personal property inventory is not used for taxes. The main benefit of keeping and maintaining it is purely organization – knowing exactly where your things are, and how much they are worth, can be very useful when your life circumstances change and you want to sell (or give away) things you no longer use or might have forgotten about. The self-service storage locker industry thrives on people making monthly payments to save things they do not regularly use!

Secondary Financial Records

Your secondary financial records are usually just bigger lists, putting together your different primary records into easy-to-read documents for your own personal reference. Usually these are reports you would put together yourself, but there are some cases where they would be automatically generated.

Income Tax Returns

After you’ve filed your income tax return, keep a copy for later reference. This also includes any receipts you have from taxes paid – these can be very important if you are audited one day. Legally you should hold on to all tax returns and receipts for 7 years, but it can be useful to keep them for longer if you want to occasionally work on long-term financial planning.

Net Worth Statement

[rich]Your net worth statement can be one of the most powerful motivators to keep control of your personal finances! Until you know where you stand, it is very difficult to make and keep realistic financial goals.[/rich] Your “Net Worth” is basically a sum of all your assets, minus all your liabilities, in one document. This is where you would add up your personal property inventory, investment values, bank balances, and cash you have squirreled away in a bunker in the desert, and subtract the outstanding balances of your credit cards, student loans, car loans, and home mortgages. This should be a one-page document you update every couple of months that helps you see your entire financial standing in one place.

Personal Expense Records

You might end up accumulating dozens of receipts in a relatively short period of time. Every few months, try to group them together and keep them in a safe place (for example, all receipts for “January – March 2016” kept in a folder in a fire-proof safe). While you do this, copy the amounts and the reason for the purchase into an excel spreadsheet. This will make it easy to know how much you spent and where you spent it for later. Plus, you can use your spreadsheet to quickly and easily find the original receipt later if you need it. By filing away all your receipts regularly, you make it less likely for any to get lost or accidentally thrown out. Doing it regularly is important to avoid a backlog (and so having to take an entire afternoon to file your receipts rather than a few minutes every few weeks).

Keeping Your Records Secure

Now that you have all of this information, your main concern is keeping it safe. Identity theft is a major problem, and if someone were to get unauthorized access to just a few of your documents, they might be able to use it against you.

Storing Paper Documents

For things like your tax returns, receipts, and investment statements, you might have paper copies that need to be both easy to find and secure. One possible route is to buy a small safe you can bolt to the floor, keeping your documents safe and all in one place. Historically, people have also rented safety deposit boxes (small ones can be about $60 a year), which is a trade-off of extreme security with inconvenience of needing to visit the bank in person and paying the annual fee.

Storing Electronic Documents

Keeping your computer files safe from hackers and phishers is a much more challenging prospect. There are dozens of ways to keep your records safe, but these are the most common rules to follow:

Rule #1: Don’t Share Your Login Information

Despite what the movies show, most “hacking” is done not by forcing complex computer algorithms to hack a mainframe, but usually just because someone shares a password with someone they shouldn’t have. This goes not just for passwords, but other information as well – never give your account numbers, credit card numbers, usernames, or passwords over the phone or by email. If you absolutely need to share a username and/or password (sharing an account with a group, for example), make sure it is a username and password you don’t use on any other websites.

Rule #2: Don’t Re-Use Your Password

You can’t tell which sites you use let the administrators see your password, and which use proper encryption. If you re-use the same usernames and passwords in many places, you’re increasing the chances that a disgruntled employee steals data and breaks into your other accounts.

Rule #3: Change Your Passwords Often

Even the most secure, unique password in the world is vulnerable to keyloggers – a type of virus software that records every key you press, and reports it back to the virus’s creator. Even if you don’t have a keylogger on your home computer (which can be hidden for months or years before “activated”, it is possible one might be on a computer lab or public computer you might access. Changing your passwords every few months is a good way to keep them safe.

Rule #4: Pick Hard-To-Guess Passwords

[rich]Some security experts recommend using a password manager. This is software that will generate extremely complex passwords for each website you need it for, then you just copy and paste with a click. [/rich]Make it hard for someone to just get into your account by guessing, or a hacker just trying random letter combinations until they get in.This webcomic illustrates how this does not mean it has to be something difficult to remember, but there is no “golden key” to making sure your passwords remain secure.

Other Financial Record Tips and Tricks

See What Account Management Services Some Financial Institutions Can Provide

If keeping track of everything is a daunting prospect, see what kinds of services your bank or other financial institution can “bundle together”. For example, it is extremely common for a person to have their savings and checking accounts, investment portfolio, home mortgage, and credit card all through the same bank, and so they are able to access all of those financial records through the bank’s online portal.

This has a strength of convenience, but there are also some serious drawbacks. For example, if you have your password stolen for this online banking service, you might lose access to everything all at once, costing a massive headache and potentially tens of thousands of dollars.

Since you aren’t shopping around for the best rates on your different accounts (high interest for your savings, low for your credit card and mortgage, and the lowest possible fees for your checking and investment accounts), you will also very likely be getting a lot “less for your money” than if you shop around separately for each service.

Visit Tax Professionals or Financial Advisers

Even if you do not do so every year, taking some time to visit with a professional can end up saving you a lot of money in the long run. For example, they can help you tell when you need to save receipts versus not, saving you a lot of time and headache in organization, and they will help you tell exactly how to use them to claim all your possible tax credits.

You might be able to remember the basics – if you have an expense that is used primarily for business, you can probably claim a tax credit on it. However, you might not know the exact process of claiming time you used your car while working, or if you can claim sales tax exemptions for new renovations on your home. Meeting with a tax professional or a financial adviser is the easiest way to navigate the seas of red tape and get the most out of your tax returns, and minimize how much time and research you need to spend on your financial records out of your own free time.

“Wealth” means having an abundance of something desirable. This can be tangible, like money and property, or intangible.

Intangible Wealth

Just because something does not have a monetary value does not mean it is worthless. Having strong connections with friends and family is often considered a major component of wealth – since these things cannot be bought or sold, they are “intangible”. Companies also have intangible wealth. For example, if the public opinion is generally positive, this is an asset the company has even though it might not be possible to assign a specific dollar value to that goodwill.

Tangible Wealth

If you can buy and sell something, then it has a tangible (meaning “can be obtained”) value. Tangible Wealth includes things like cash, bank deposits, property, stocks, bonds, and more.

Monetary VS Non-Monetary Assets

When you are building wealth, you want to start building up your assets, both monetary and non-monetary. Your “Monetary” assets are the ones that will be part of your spending plan – how much cash you have in the bank, how much income you are going to get next month, and how much money you currently have in your emergency fund. Since we can spend these funds on a very short notice, they are also called “Liquid Assets”. Stocks and bonds, which are less liquid, are also considered “monetary assets” because you will almost always know their exact value in dollars.

Your “Non-Monetary Assets” are less liquid – you usually cannot spend them directly, and it takes some significant time to do so. This includes things like property, furniture, machines, and vehicles. All of these items are useful and definitely have some value, but until you actually need to sell them you might not know exactly how much cash you can convert them in to.

Both of these contribute to your total wealth. For most people, their “non-monetary” assets will be the biggest chunk of their total wealth, usually counted as their car, house, property, and stuff they own.

Building Wealth

The idea of “Building Wealth” is referring to tangible assets. This means building up reserves of cash, bank account balances, and investments like stocks and bonds. Building up assets is a lifetime goal, usually accumulating bit-by-bit with sound personal finance strategies. By using techniques and tools like Budgeting, using a Spending Plan, and Investing, people can “put their money to work” and start earning more than just their base salary.

Financial Goals

[rich]Download this sample spending plan, and fill it with your own spending patterns. Then try to make a financial goal for the next 3 months, and find ways to adjust your spending plan to hit your target! [/rich]

Setting, and keeping, financial goals is one of the keys to building wealth. For example, a starting goal to kick-start your investments would be to find a way to save up $300 to use to buy your first stocks. To do this, you can take a look at your spending plan, and identify places where you can trim off a few dollars each month from your variable (and sometimes fixed) spending, and see how quickly you can reach your goal.

By having these goals, it gives an extra incentive to keep control of your spending, which is a major key to maximizing your savings and building up assets.

Trading Strategy: Investing for the first time in the stock market is very overwhelming; even if it is done with virtual money. I’ll start saying that implementing a strategy takes a lot of practice and patience. You must begin understanding some of the “tools” and “terms” involved. Without this basic knowledge, it is difficult -if not impossible- to practice your new skills properly.

At first I didn’t know where to start, so I decided to see the most active stocks and the biggest gainers, because I believe that learning from the best stock market winners can guide me to tomorrow’s leaders. After I had some training ideas, I decided to do a fundamental analysis. I looked carefully at a company’s earnings, earnings growth, sales, profit margins, and return on equity among other things. Doing this analysis definitely helped me to narrow down my choices.

I always like to keep in mind some great clichés “The trend is your friend”, “buy low and sell high” and “buy high and sell higher”. When I had a couple of stocks ready to trade, I made sure they where diversified and they where from the leading industry groups or sectors. I noticed that the majority of past market leaders were in the top industry groups and sectors.

Another strategy that I used was to track the general market given that most stocks usually follow the trend of the general market. The general market is represented by leading market indices like the S&P500, Dow Jones Industrials, and the NASDAQ Composite.

When I had my portfolio ready, this was just the beginning. Even though I didn’t check my portfolio every 2 hours or every single day, at least 3 times a week, I read the latest news about the stocks I bought and about the market in general. After that, I also checked the chart price and volume action, this helped me recognize when a stock has reached its top and It helped me decide if I should sell my stock or not. Finally, I always made a post-analysis of my stock market trades. That way I could learn from my successes and mistakes.

When we think of money, stored value means anything that isn’t cash, but you can still use to transfer value – checks, debit cards, gift cards, and forms like that. These are used to transport some dollar amount which we can later exchange for goods and services.

Each of these forms of stored value have their advantages and disadvantages, along with some properties that make them unique.

Difference between “Stored Value” and Money

Money itself is created as debt in the Federal Reserve (Click Here for details), but it only really exists as a concept. Money has value because we all agree it has value, and so we can use it as a medium of exchange. Forms of Stored Value simply are a storage system for money, meaning they do not have any value in and of themselves. This means that if you write me a check, I only think that check has value if I can exchange it directly for cash. If I do not think you have enough money in your bank account to cash this check, then I probably am not going to assign it very much value.

Types of Stored Value

Checks

Checks might be the oldest form of stored value. This is a piece of paper with instructions to your bank to pay the person you specify some amount.

A check will have your account number and bank routing number, along with who you are writing the check to, the amount of the check, the date, and your signature. It may also have your name and address, and a place to write a “Memo”, or a note about what the check is for. In the simplest terms, when you give someone a check, they take it to their bank, who then uses the bank routing number to contact your bank, and your account number to specify your exact account. Your bank then confirms your signature, and withdraws the amount of the check from your account and transfers it to the other person’s account at the other bank. The check is then “cancelled”, so it cannot be used again, and the cancelled check is returned to you showing that it has been processed.

This allows you to send any amount of money from your account to anyone else who has a bank account. Some check-cashing services also offer to convert checks directly into cash (for a fee) for people who do not have a bank account.

If you have a check that you want to convert into money to spend, there are a few ways of doing it, each with their own advantages and disadvantages.

Deposit into your own bank account – this usually does not have any fees, but there is usually a few days of processing time before you can access the funds.

Cash at a bank – Your bank might be willing to convert your check to cash if you have an account that has enough funds to “cover” the check in case it turns out to be invalid. If you don’t have a bank account, the bank that issued the check will usually cash it for a fee (usually a fixed amount).

Check cashing services – These servicies used to be more popular when it was less common for individuals to have bank accounts. A check cashing service will convert a check directly into cash, usually charging a percentage fee. There is typically a maximum amount they will be willing to cash. This is often the quickest option to convert your check into cash, but is also the most expensive.

Advantages of using checks

Checks can be very handy when you need to make payments in the future, since you can write a “post-dated” check that only becomes valid at a certain point in the future. For example, you can send your land lord 12 post-dated rent checks instead of mailing new checks every month. This can also let you write a check in advance of payment, with the ability to cancel the check (i.e. tell your bank not to honor it) based on certain conditions.

Disadvantages of checks

Writing checks requires a checkbook, which very few people want to carry around most of the time. Since checks are only validated using a signature, check fraud (people passing fake checks as genuine, or editing the amounts on a genuine check to be a greater amount) has historically been a major cause for concern.

Checks also take time to “clear”, or have the money transferred from your bank to another. This means that if you have any outstanding checks, you need to constantly reconcile your bank account to subtract any outstanding checks to know your “true” balance.

For businesses, taking checks can be risky, and very few still do. This is because it is impossible when receiving the check to know that the person giving it actually has the funds in their bank to make the payment. Another problem of check fraud was people writing checks that they knew were unable to be cashed, often in other towns, leaving the businesses very few ways to recover their losses. Local businesses would often refuse to take any checks from non-local banks for this reason.

Money Orders and Cashier’s Checks

Money orders are a lot like checks, in fact they look almost identical. However, a money orders and Cashier’s Checks are issued by a large corporation on your behalf – cashier’s checks by a bank, money orders by post offices, currency exchanges, and other such institutions.

Money orders are most commonly used by people without bank accounts to pay bills to institutions which do not accept cash (most companies that you would pay by mail will not accept cash).

Cashier’s checks are most often used where check fraud is a major concern. Paying for large purchases (or paying the government in taxes) might request a cashier’s check.

Both of these formats effectively serve for you to convert your cash into a format that is more secure to send by mail, and more secure for businesses and others to accept. However, both are less useful if you have your own checking account in good standing.

Debit Cards

Debit cards are very similar to checks, and are usually tied to your “checking account”. The biggest difference is that all payments are controlled electronically, usually instantly. Debit cards can be used in most places where credit cards are accepted.

In place of the signature of a check, you instead need to input a PIN number to verify your identity and authenticate the purchase. Debit cards may or may not be used for online transactions, depending on your card issuer.

Debit cards evolved from ATM cards, which were originally only used at ATM machines to withdraw cash and check bank balances. They operate using a magnetic stripe that contains your bank information, which is processed using a card reader by the business you are buying from. In most of the world, and increasingly in the United States, debit cards also come with a chip, which has more security features and is more difficult to steal than a magnetic stripe.

Advantages of Debit Cards

Debit Cards were developed to fill a similar role to checks, without the drawbacks. You can still pay directly from your checking account, and the seller will know immediately that the funds were transferred, eliminating the biggest problems of check fraud. The pin system is also more secure than a signature, both because the seller knows right away that the card is in the hands of its rightful owner, but also for the card holder because it is much less likely that someone else will be able to pass off another debit card as your own.

Disadvantages of Debit Cards

Debit cards can still be counterfeited, although this is much less likely with the varieties with a chip. It is also possible that debit payments may not appear in your account right away, payments may appear instantly, or be delayed by up to a week. This means that debit card users are less likely to keep a detailed record of all debit transactions, and may be surprised later when transactions they forgot about appear in their account.

This can make it possible to over-draw your account, which typically comes with heavy fees from your bank.

Stored Value Cards

Stored value cards are usually issued by a credit card company or bank, and are often given as gifts. They are also sometimes called “Prepaid Cards”. To use a stored value card, you need to “Charge” it by adding value (either using cash at a kiosk for the card issuer, or sometimes online by transferring value from your bank account). Once it is stored, you can use a stored value card any place you would use a credit cards. The card issuer may charge a fee to use these services.

Advantages of stored value cards

Stored value cards can be a great way for people without a credit card to make online transactions, since you can make payments in the same way as you would with a credit card. They are also often used as gifts as a “use it anywhere” gift card. Generally speaking, stored value cards work as a more flexible form as cash.

Disadvantages of stored value cards

Like cash, stored value cards can be easily lost or stolen. Since they are not tied to you in any way (and are normally given as gifts), whoever is currently holding the stored value card controls all the value it has. This makes them very risky to use for larger amounts.

The card issuer also usually charges a fee to use the card, and if you maintain a balance, they may charge “storage fees” as well.

Gift Cards

Gift Cards are another form of stored value. Many stores and online retailers will let you convert cash into a gift card which you can use in their store. Gift cards usually have no fees, so they retain their value longer than other stored value cards. The major drawback is that you can only use a gift card at the business which issued it. For some businesses, like Amazon.com ([hq]AMZN[/hq]) this is not really a limit, but for restaurants and individual retailers it might be.

As their name implies, a “Gift Card” is typically given a as a gift. Due to their limiting nature, it is very rare to purchase and use a gift card for yourself.

Advantages of Gift Cards

Gift cards are great to give as gifts. Because they can only be used in one location, they are less prone to theft and loss as other stored value cards.

Disadvantages of Gift Cards

The major drawback of gift cards is that they can only be used where they were issued, so they typically are not used by individuals as part of their main “wallet” of stored value. However, they do get a lot of use around the holidays!

Note about Credit Cards

Unlike these other items, credit cards are NOT a form of stored value, and do not act as money. This is because credit cards are a loan (or a form of “credit”). When you make a purchase from a using a credit card, no value is being transferred from you to the place where you are spending. Instead, you are creating a debt that you must later pay back with interest (usually no interest until a few weeks has passed).

In contrast, when you use any of these other forms, value is being directly transferred from you to the person you are paying. There is no loans or credit acting as a “middle man” – it is a direct transfer of money from one person to another.

Bitcoins and Other Virtual Currencies

Bitcoins and virtual currencies have become very popular in the last few years, but it is not always easy to tell if they are a form of money in and of themselves, or they are just a stored value of money. Their actual definition shifts based on how you, the consumer uses them.

For example, if you convert your dollars into bitcoins, then visit a shop that lists their prices in bitcoins and accepts bitcoins as payment, it is acting like money directly. However, if that shop lists all their prices in dollars, but they take bitcoins as payment with a conversion rate, then your bitcoins are just acting as a ‘stored value’ for dollars.

To make things more complicated, you can also buy a bitcoin because you think its value will go up over time. This means that you are treating it not as stored value or money, but as an investment, and are using “speculation” to try to turn a profit.

A “Spending Plan” is exactly as it says – a plan of what you will be spending each month. There are usually two parts – your “fixed” spending and your “variable” spending. The fixed part is usually the same every month, with things like rent/mortgage payments, grocery bills, insurance, and car payments. The variable part changes a lot from month to month, and can include things like Christmas shopping, buying new furniture, and paying for repairs.

You can then balance what you need to spend for the month with your take-home pay, and use whatever is left over to allocate as you wish – going out to the movies, adding to your investments, or keeping in your savings account.

How is a Spending Plan different from a Budget?

Spending Plans and Budgets are similar in a lot of ways – you’re making a list of your expenses in order to allocate your income. The biggest difference is that when you make a budget, you are allocating how you are going to spend just about every dollar you earn – take a look at our Home Budget Calculator and see how many settings you need to make!

https://youtu.be/uzrHIiP72CU

Pictured: the burrito that broke your budget

A budget also gives you allowances that you cannot go over. For example, you might have a $150 food budget for yourself while you are in college each month, assuming that you will be buying groceries and cooking nearly every meal yourself. If you end up going out with friends a few times more than expected for burritos, you might go ‘over budget’, and you know that you will have to take that money from somewhere else in the budget to make it work.

A Spending Plan, on the other hand, is much more simple. You make your list of fixed, hard expenses that do not change from month to month, and then each month you add your other essential expenses. This means you are left with your ‘discretionary income’, or the money you can spend on whatever you like. If you want to use your discretionary income on a few extra trips for burritos, go right ahead! This only means you have less to spend on other discretionary expenses, not that you went ‘over budget’ and need to start from scratch.

Spending Plan Terms

Fixed And Variable Spending

When you are separating your spending between “fixed” and “variable”, your rule-of-thumb should be that if you need to change an item month-to-month, it should be part of your variable spending, whereas if it is something you don’t have the ability to change easily, it should be part of your “fixed” spending.

[rich]Add how much you spend on clothes and fashion to your spending plan. This helps you visualize how much you value your style versus other essentials! If you skip one $60 shopping trip per month, that will add up to $720 per year![/rich]This also means that when you want to start controlling your spending habits to increase your savings and build wealth, any spending you can reduce from your “fixed” expenses will have a bigger, long-term impact. For example, if you decide to move into a new apartment, a $50 difference in rent will not make a huge difference in your per-month spending, but it adds up to over $600 per year. In contrast, if you skip out on a variable expense, like a dentist appointment, you might get a one-time savings, but it will make a big impact on your long-term strategy to build up your savings, investments, and wealth.

Income

When you are building your spending plan, it is essential you specify how much you are earning each month as your take-home pay (how much you actually deposit in the bank), not your salary, or pre-tax income. This way you can build an honest, realistic plan based on what money you actually have at your disposal.

Savings and Investments

Your savings and investments are also extremely important in a spending plan, but where they fit in will change over time. For the first few months of using a spending plan, your savings and investment will be what is ‘left over’ from all your other discretionary expenses.